Tax policy update

Senate Committee Substitute for HJR 173: Same Tax Swap, Bigger Loopholes

Listen to this article

Prefer audio? You can listen to the full article here.

Article Audio

Open audio in new tabThe Senate Committee Substitute for HJR 173 does not fix the core problem with this proposal. It still asks Missourians to surrender constitutional protections first and trust future lawmakers to write the real tax plan later. In some places the new language looks cleaner. In several of the most important places, however, it is either still too weak to protect citizens or actually worse than the House version.

Bottom line first

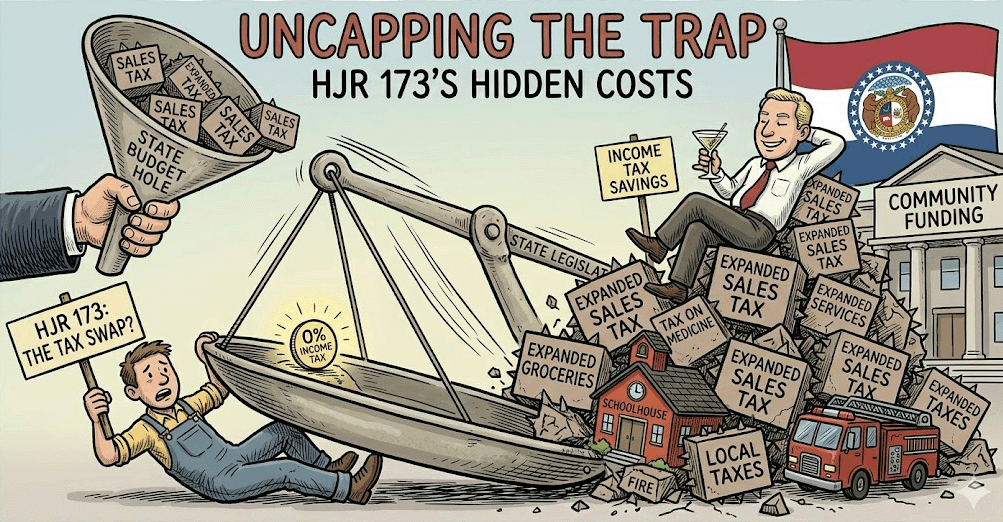

This is still not a straight tax-cut plan. It is still a constitutional framework for replacing one tax burden with others, including broader taxes on goods and services, while suspending key constitutional protections for future enabling legislation. The Senate version even stretches one of those special carve-outs from three years to five years.

How to use this page

This article is built for two audiences at once: people who follow Missouri policy closely and people who simply want to understand what changed. Use the jump links below to go straight to the part you care about.

Quick take: what changed, in plain English

One change looks tougher

The House version said qualifying future tax legislation only had to be “anticipated” to help eliminate income tax. The Senate substitute changes that to say lawmakers must find it “will” do so. That sounds stronger, but it still allows the claim to be made indirectly and does not require a strict dollar-for-dollar, same-bill offset.

One change is clearly worse

The Senate substitute expands the special carve-out window for Hancock Section 18(e) and the transportation-fund protections from three years to five years. That gives future lawmakers more time to act under the constitutional loophole.

The trigger language got riskier

The new trigger baseline compares a full fiscal year of General Revenue against only the first half of FY2027. Standing alone, eliminating the personal income tax faster would not be the problem. Lawmakers could still cut that tax by statute if they were truly just using growth or real spending restraint. The problem is that this HJR pairs that aggressive trigger with new constitutional permission to expand taxes to goods and services later, while the fiscal note shows the size of the hole this could create in future budgets if lawmakers keep trying to preserve high spending.

The core problem remains

The plan still says, in effect: approve the constitutional authority now, and lawmakers will decide later what to tax, how much to tax, what exemptions to include, and how to make the math work.

What changed from the House version to the Senate Committee Substitute

Here are the most important language changes and why they matter.

| Issue | House version | Senate substitute | Why it matters |

|---|---|---|---|

| Income-tax trigger baseline | Compared annual General Revenue to FY2025 collections, adjusted for inflation. | Compares annual General Revenue to collections “as of January first of the 2027 fiscal year,” adjusted for inflation. | The new baseline is effectively a half-year benchmark. The fiscal note says that makes the trigger much easier to hit and could eliminate the individual income tax by 2028. |

| Definition of qualifying legislation | Legislation only had to be “anticipated, directly or indirectly” to lead to income-tax elimination and lower local taxes. | Now says the legislation “will directly or indirectly” lead to that result. | That sounds better, but still does not require a strict same-bill offset, a lockbox, or a concrete measurable formula the public can verify ahead of time. |

| Local tax adjustments | Political subdivisions had to adjust annually. | Adjustment frequency is now “in the manner and the frequency provided by law.” | This gives future lawmakers more discretion and leaves more unanswered until enabling legislation is passed. |

| Constitutional sales-tax adjustment | Tied to a historical three-year revenue median, adjusted for inflation. | Tied to the amount produced by future sales-tax base expansion, with details to be provided by later law. | This is a major rewrite. It moves the mechanism away from a fixed historical benchmark and toward future legislative design. |

| Special exemption window | Three years. | Five years. | This is a significant expansion of the period during which lawmakers could use the Hancock and transportation carve-outs. |

The one sentence version

The Senate substitute cleaned up a few words, but it still keeps the same basic deal: give lawmakers constitutional permission first, and let them show you the tax plan later.

What still has not changed

- The amendment still allows state and local sales and use taxes to be expanded to transactions involving any goods and services for the stated purpose of eliminating the state individual income tax and reducing local tax rates.

- The amendment still requires political subdivisions to offset extra revenue from any future sales-tax-base expansion, but it leaves the details to later legislation.

- The amendment still exempts qualifying legislation from Section 18(e) of the Hancock Amendment.

- The amendment still exempts qualifying legislation from Article IV, Sections 30(b), 30(c), and 30(d), the transportation-related provisions you have already seen raised in testimony.

- The ballot language still does not tell voters plainly that this opens the door to taxing currently untaxed services and transactions later.

Why the loopholes still matter: examples people can understand

Supporters will point to a few tightened phrases and say the Senate substitute is now safer. But the holes are still there. Here are a few simple examples.

Example 1

The “will directly or indirectly” problem

Suppose lawmakers pass a bill expanding taxes to services and say the extra revenue will indirectly help reduce the income tax. That is still not the same as requiring that bill to deliver a hard, same-bill, dollar-for-dollar cut that the public can see and verify. “Indirectly” leaves room for broad claims and future promises.

Example 2

The missing plan problem

If lawmakers truly knew exactly what they wanted to tax and by how much, they could put that plan in front of the public now. Instead, the amendment still asks voters to approve the authority first, while the actual service list, exemptions, rates, and offsets all wait for later legislation.

Example 3

The five-year loophole

Under the House version, qualifying legislation had three years to use the special Hancock and transportation carve-outs. The Senate substitute stretches that to five. That is two more years for future lawmakers to act without the normal constitutional check that would otherwise apply.

Example 4

The service-tax door is still open

The substitute did not restore the constitutional protection against expanding taxes to services. That means the core constitutional surrender is still the same. The people are still being asked to give up that protection first.

Why they are doing this as a constitutional amendment

This remains one of the most important points.

If lawmakers truly wanted to eliminate the personal income tax only through revenue growth, they could keep reducing it by statute as real growth actually occurs. They do not need a constitutional amendment to do that.

What they do need a constitutional amendment for is something else: they need voter approval to get around the constitutional protections that currently block the expansion of sales and use taxes to services and other transactions that were not taxed before. The text still says that, notwithstanding the existing constitutional protection, state and local sales and use taxes may be expanded to transactions involving any goods and services for the stated tax-elimination purpose.

What citizens are being asked to give up

The public is not just being asked to approve a lower income tax. It is being asked to give lawmakers constitutional permission to expand taxes to services and other currently protected transactions later, while also letting those future bills avoid key constitutional guardrails for up to five years.

A quick note on Section 18(e)

Opponents of our position have become very picky about calling Section 18(e) part of the “Hancock Amendment.” Technically, Section 18(e) was added later, in 1996, while the original Hancock Amendment dates to 1980. But Missouri official legislative materials still describe current Article X tax-and-revenue limits, including Section 18(e), as provisions “commonly referred to as the Hancock Amendment.” So when we use that shorthand, we are using the language most Missourians already recognize, even though some people prefer to distinguish the later 1996 voter-approval language from the original 1980 amendment.

Why the Section 18(e) issue is still central

The Section 18(e) issue is still not solved. In fact, the special carve-out now lasts longer.

Whether someone calls Section 18(e) part of the Hancock Amendment, part of the 1996 voter-approval amendment, or something else entirely, the practical meaning is the same: if lawmakers later pass tax-base-expansion legislation under this amendment, the people are not just being asked to trust that lawmakers will do the right thing. They are also being asked to trust them after having suspended one of the constitutional protections that would otherwise force stricter public accountability for new annual revenue.

That is why this remains a structural objection, not a minor drafting concern.

What Section 18(e) says

“Any proposed law or amendment to the constitution submitted to the people by the general assembly, which would increase taxes, fees, or revenues above that authorized by law on November 4, 1980, shall require approval by a majority of the qualified electors voting thereon.”

In plain English, Section 18(e) means that when lawmakers want to raise taxes or bring in more revenue beyond what the law already allowed, they normally have to take that proposal back to the people for approval.

That is why this matters in HJR 173. The amendment says that if future legislation is passed under this framework within the special carve-out window, it “shall not be considered new annual revenue for purposes of Section 18(e).” In other words, lawmakers are trying to make sure those future tax changes do not trigger this voter-approval protection.

So the concern is not just that voters are being asked to approve a constitutional framework now. It is that, after doing so, they could lose one of the protections that would otherwise require lawmakers to come back and get voter approval for later revenue-raising legislation.

What the new fiscal note tells us

The new fiscal note is one of the strongest warnings in the whole record.

- It says the substitute’s new trigger structure could drop the individual income tax rate to 3.1% in tax year 2026, 1.5% in 2027, and 0% in 2028.

- It estimates General Revenue losses of about $4.18 billion in FY2027, $6.25 billion in FY2028, and $8.51 billion in FY2029.

- It says expanding the sales-tax base is not required to eliminate the income tax, but if enacted it could speed up the elimination.

- It confirms that the transportation carve-out would allow increased sales taxes on motor vehicle sales to go to General Revenue instead of the usual transportation-related distribution path, if qualifying legislation is enacted within five years.

What that suggests

The substitute still looks less like a clean tax-cut proposal and more like a framework for finding and redirecting revenue in new ways while trying to preserve high spending commitments. The text itself and the fiscal note do not prove motive, but they do show a structure built for future revenue replacement rather than for immediate spending restraint.

The business-case problem

Another major weakness in the push for this amendment is the competitiveness argument. A central sales pitch has been that Missouri must do this to compete with no-income-tax states.

But growing business opposition undercuts that claim. Associated Industries of Missouri has argued that Missouri already compares favorably with no-income-tax states on several important measures: lower cost of living, lower corporate tax rate, and stronger business creation in 2024 and 2025 than almost every no-income-tax state, according to analysis prepared by that organization. The Missouri Independent also reported McCarty’s argument that Missouri’s current business tax burden, as a share of total state and local taxes, is already lower than every state without an income tax.

Why that matters

If the main policy argument is “Missouri has to do this to stay competitive,” and major business voices are saying Missouri is already highly competitive without this amendment, then one of the amendment’s biggest justifications starts to collapse.

That does not mean Missouri should never cut taxes. It means lawmakers have not proved that rewriting the Constitution, surrendering service-tax protections, and expanding Hancock carve-outs is necessary to keep Missouri economically competitive.

The better path is still the obvious one

If Missouri wants to lower taxes honestly and sustainably, the better path is still the same one Act for Missouri has been pointing to from the beginning:

- Decide what government should actually cost.

- Cut spending where it exceeds the proper role of government.

- Use real, measurable savings to reduce taxes by statute.

- If lawmakers want to replace one tax with another, show the people the full plan before asking them to alter the Constitution.

Growth is speculative. Spending cuts are measurable. This amendment still asks the people to approve the structure first and trust that the real plan will be reasonable later.

Final recommendation

Act for Missouri recommendation

OPPOSE

The Senate Committee Substitute still fails the most important tests. It still seeks constitutional permission to expand taxes to services and currently protected transactions. It still leaves the real replacement-tax plan to future legislation. It still suspends key constitutional protections for qualifying future laws. And it now extends one of those special carve-outs from three years to five.

Missourians should not be asked to surrender constitutional protections first and hope lawmakers provide a fair plan later. If the plan is good, lawmakers should show it to the people now.

Learn more

Related articles and background

Missouri’s Income Tax “Elimination” Plan Is a Tax Swap

A broader look at how this proposal evolved and why critics say it is not a simple tax cut.

What Is Missouri Proposition C — and Could HJR 173 Change How It Works?

Explains the statewide 1-cent school sales tax and why HJR 173 could matter to dedicated-fund structures later.

Clearing the Chatter on HJR 173

A fact-based guide separating what the bill actually says from what supporters hope future legislation might do.

What the Senate Hearing on HJR 173/174 Confirmed

A recap of the first Senate hearing and the structural concerns that still remain.