Taxation | Constitutional Amendment | Missouri 2026

Listen to this article

Audio version

Prefer to listen instead of read? Use the player below for the narrated version.

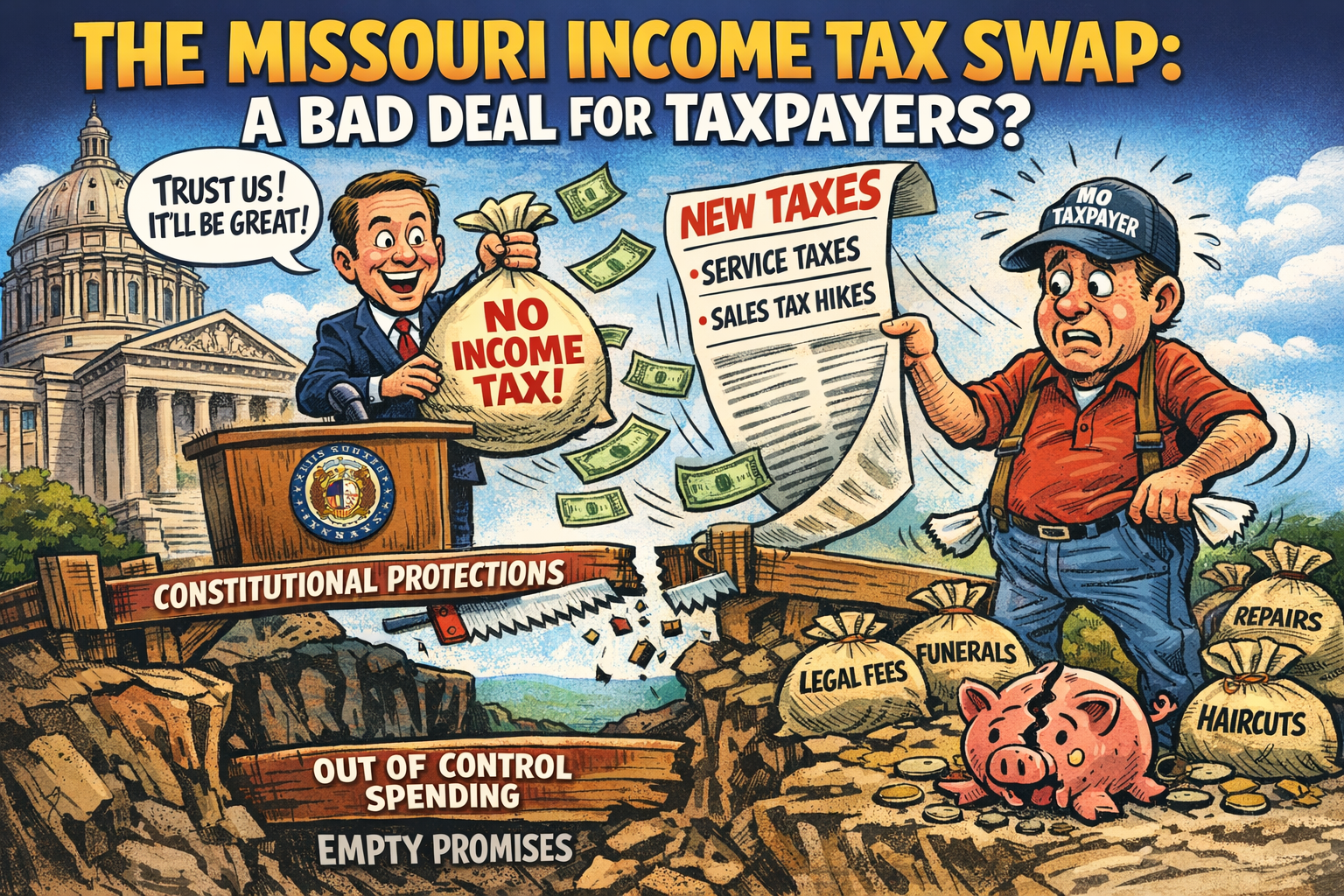

Missouri’s “Income Tax Elimination” Plan Is Really a Tax Swap

The first thing Missouri voters should understand is this: HCS HJRs 173 & 174 does not automatically eliminate the personal income tax, and it does not itself impose a tax on services. What it does do is change the Constitution to remove current protections and give future lawmakers the power to expand sales and use taxes to goods and services that are not taxed today.

To be fair, the latest version — HCS HJRs 173 & 174 — is more restrained than Speaker Patterson’s earlier drafts. It narrows some of the constitutional carve-outs, drops some of the broader implementation language, and replaces the vaguer trigger framework with a more specific formula. But the core structure remains: it still opens the constitutional door to broader sales and service taxation, still relies on future promises of income-tax relief, and still asks voters to trust lawmakers to exercise powers they have not shown much discipline in using.

Editorial note

This article compares the three texts provided for review: Patterson's first try (HJR 165), Patterson's second try (HJR 174), and the substitute text that just passed out of the House HCS HJRs 173 & 174. This article follows the actual text we reviewed and the official House bill pages linked below.

Simple repeal?

No

The current text is not just “end the income tax.” It also rewrites constitutional rules on sales, use, and related transaction taxes.

Door to service taxes?

Yes

The old protection stays on paper, but the amendment creates an override allowing future legislation to tax transactions involving “any goods and services.”

Constitutional carve-out?

Yes

If qualifying legislation is enacted within three years, the amendment gives it special treatment under Section 18(e) and selected transportation-related provisions.

Real solution?

Cut spending first

If Missouri wants lower taxes, the durable path is budget restraint and statute-based cuts, not a constitutional permission slip to tax more transactions first.

The shortest version

This proposal started as a simple-sounding plan to eliminate the personal income tax. It evolved into a broader constitutional framework that could let future lawmakers expand transaction taxes to currently untaxed goods and services, use soft “anticipated” findings to justify those expansions, and take advantage of a three-year constitutional exemption window.

Why ordinary Missourians should care

When politicians say “let the people decide,” the people deserve the whole deal. Voters should be told plainly that this is not just about the income tax. It is also about future tax authority, constitutional protections, local tax adjustments, and whether a state that has not controlled spending should be given more room to reshuffle the burden.

Part 1

How we got here

The opener

Keep the 2015 anti-service-tax language in subsection 1, then immediately carve around it in subsection 2.

- Allows future legislation to expand taxes to any goods and services.

- Ties that expansion to the stated goal of reducing and eliminating the personal income tax.

- Creates a broader constitutional carve-out from Sections 18 and 18(e), plus Article IV sections 30(a)-30(d).

The expansion

Adds the promise that no personal income tax would apply once statutory triggers push the top rate below 1.4%, starting in 2031 or later.

- Adds the “anticipated, directly or indirectly” legislative-finding language.

- Automatically sweeps local and constitutional sales taxes onto the broader base.

- Gives the Director of Revenue special authority to define terms and police “circumvention.”

The cleanup without the cure

Removes some of the most obvious overreach, but keeps the core tax-swap architecture in place.

- Writes a growth formula into the constitution instead of leaving triggers entirely to statute.

- Keeps the authority to expand taxes to any goods and services.

- Narrows the carve-out to Section 18(e) and Article IV sections 30(b)-30(d), but does not eliminate the carve-out.

| Question | HJR 165 | HJR 174 | HCS HJRs 173 & 174 |

|---|---|---|---|

| Allows future taxation of “any goods and services”? | Yes | Yes | Yes |

| Keeps anti-service-tax language but overrides it? | Yes | Yes | Yes |

| Uses soft legislative findings instead of a hard dollar-for-dollar swap? | Not defined as clearly | Yes | Yes |

| Creates a constitutional carve-out for qualifying tax increases? | Yes, broader | Yes, broader | Yes, narrower but still real |

| Adds extra agency power to define terms and prevent circumvention? | No | Yes | No |

Part 2

What changed - and what did not

What changed

- The current text replaces the vague “whatever triggers the legislature creates” approach with a written formula based on net general revenue growth above an inflation-adjusted FY2025 baseline.

- It removes HJR 174's automatic sweep-in language for all local and constitutional sales taxes.

- It drops HJR 174's special Director of Revenue definition and anti-circumvention subsection.

- It narrows the constitutional carve-out compared with the earlier drafts.

What did not change

- The amendment still overrides the constitutional protection against expanding taxes to services or transactions not taxed on January 1, 2015.

- The amendment still lets future legislation impose taxes on transactions involving any goods and services.

- The “purpose” test is still soft enough that lawmakers only need to state a finding that the legislation is anticipated, directly or indirectly, to lead to eliminating the income tax and reducing local tax rates.

- The amendment still contains a three-year special constitutional treatment window for qualifying tax increases.

Part 3

Deep dive: the core concerns are still there

1) Does the current text still open the door to taxing services?+

Yes. The amendment keeps the old protective sentence in Section 26.1 saying state and local sales and use taxes shall not be expanded to tax services or transactions not taxed on January 1, 2015. But the next subsection overrides it with the phrase “Notwithstanding any provision of this Constitution to the contrary, including the foregoing” and authorizes future legislation to tax transactions involving any goods and services.

Plain-English translation: the protection remains on paper, but the amendment creates a constitutional exception that future lawmakers could use to get around it.

That means it is not accurate to claim the amendment only affects a narrow, defined list of “small” personal services. The text does not create that limiting list. It leaves the actual line-drawing to future legislation.

2) Does the phrase “for the purpose of reducing and eliminating the state individual income tax” really protect voters?+

Not very much. The current text does not require an immediate, dollar-for-dollar swap. It says qualifying legislation is legislation that expressly states the General Assembly's finding that it is anticipated, directly or indirectly, to lead to eliminating the income tax and reducing local tax rates.

That is much softer than requiring an automatic income-tax cut in the same bill. In practice, it means a future legislature could broaden taxes on services and justify it with a finding that the change is expected to help the long-term elimination effort.

The core weakness: the amendment does not force a hard tax swap. It allows future lawmakers to claim one.

3) What does the three-year constitutional carve-out really do?+

The current text does not suspend all of Hancock for three years. That would be too broad. What it does is narrower but still serious: if the implementing legislation is enacted within the first three years after the amendment takes effect, any resulting tax or revenue increase is exempt from Section 18(e) and from Article IV, Sections 30(b), 30(c), and 30(d).

The earlier drafts were broader. They attempted to bypass Section 18 and Section 18(e), plus more of the Article IV transportation provisions. The current text retreats from that, but it still creates a targeted constitutional escape hatch for qualifying tax increases enacted during the three-year window.

Best precise wording: this is not a full repeal of Hancock; it is a limited three-year exemption window for qualifying implementation bills.

4) Why go through a constitutional amendment at all?+

If all lawmakers wanted was a statutory formula that reduces the income tax when revenue grows, they likely could have pursued that in ordinary legislation. Missouri has already used revenue-trigger laws to reduce the top rate over time.

The part that needed constitutional change was the part ordinary legislation could not do by itself: override the current constitutional protection against expanding taxes to untaxed services and transactions, and create special constitutional treatment for qualifying tax increases passed in the first three years.

That is why it is fair to say this HJR vehicle was not necessary merely for the “growth formula.” It was necessary for the broader rewrite.

5) Is the ballot language fair and complete?+

The current ballot summary says the amendment would:

- phase out the individual income tax based on revenue growth,

- reduce personal property tax and other local tax rates,

- modernize the sales and use tax, and

- protect local funding for public schools.

That language is politically polished. What it does not tell voters plainly is that the amendment would also create a constitutional override for future taxation of transactions involving any goods and services, or that qualifying implementation bills enacted within three years get special constitutional treatment.

Our view: if legislators truly want the people to decide, then they should tell the people the whole deal up front - not just the most popular talking point.

Fiscal note

What the fiscal note quietly confirms

Read the fiscal noteThe fiscal note does not say this proposal cannot be scored. It does provide major estimates, including substantial General Revenue losses as the income tax phases down and eventual multibillion-dollar impacts at full implementation.

What it also says is just as important: some of the most significant downstream effects cannot yet be precisely measured because the enabling legislation has not been written. In other words, voters are being asked to approve the constitutional framework first, while many of the real tax details would be decided later.

The fiscal note also confirms that expanding sales and use taxes to additional goods and services is not required to trigger the income-tax phaseout, but that it could speed it up. That means broader taxation of goods and services is not simply an unavoidable technical feature of the plan. It is an added power the amendment would give future lawmakers.

That is why the real policy question is not just how to replace the income tax. The real question is whether Missouri has first decided what state government should actually cost. Until that question is answered honestly, any discussion about “eliminating” one tax risks becoming a debate over which other taxes should be expanded to sustain current spending.

The better order is the simpler one: determine what government truly needs to spend, reduce the budget where it should be reduced, and then decide the most honest and sustainable way to pay for what remains. This proposal largely reverses that process by asking voters to approve new constitutional tax authority before the spending problem has been seriously addressed.

Part 4

The real problem is spending

Missouri's operating budget trend

Pre-COVID growth was real but gradual. The major surge came later. From FY2016 to FY2019, Missouri’s recommended operating budget grew roughly 10% on an all-funds basis. From FY2019 to FY2026, it grew roughly 84%.

General revenue versus the income-tax target

Missouri still depends heavily on the personal income tax. That is exactly why spending discipline matters so much. You cannot honestly promise major permanent tax relief while defending a permanently elevated spending base.

What prior income-tax cuts show

Missouri has already been reducing the top individual income-tax rate. The top rate is 4.7% for tax year 2025. But official fiscal scoring of the 2022 rate-cut package treated those reductions as losses to General Revenue, not as self-financing gains.

That does not prove growth never happens. It does show that “growth will pay for it” is not something the official fiscal note treated as a guaranteed replacement plan.

What a more honest reform path looks like

If Missouri returned the FY2026 general-revenue recommendation of about $15.70B to an inflation-adjusted FY2019 level of roughly $12.01B, that would free about $3.69B.

That is real money. But it still covers only about 40% of the roughly $9.17B-$9.25B personal-income-tax stream. That means the serious path is budget restraint first, staged tax cuts second - not a constitutional tax-swap that gives future lawmakers new ways to tax services.

The budget argument in one sentence

Growth is speculative. Spending cuts are measurable. If lawmakers want lower taxes, they should first prove they can shrink the size of government instead of asking voters to weaken constitutional protections and trust them later.

Part 5

A better argument for lower taxes

What to reject

- Do not call this a clean tax cut.

- Do not pretend the service-tax question is settled or narrowly defined by the amendment text.

- Do not treat a soft “anticipated, directly or indirectly” finding as a binding guarantee.

- Do not tell voters this is only about letting them decide on income-tax repeal.

What to demand instead

- Real budget-cut targets first.

- Transparent statute-based rate reductions tied to actual savings, not just hoped-for growth.

- No expansion to taxing services unless voters are told that plainly and specifically.

- No special constitutional exemption windows for implementation bills.

Part 6

Glossary and citizen guide

Hancock vs. Section 18(e) vs. “Carnahan”+

People often use “Hancock” loosely for Missouri's taxpayer-protection structure. The current text does not suspend all of Hancock. It creates a narrower carve-out tied to Section 18(e) and selected Article IV transportation provisions. That is why careful wording matters here.

Sales tax vs. use tax+

Under current Missouri law, sales tax generally applies to tangible personal property and specifically listed taxable services. Use tax generally applies to the storage, use, or consumption of tangible personal property in Missouri when Missouri sales tax was not paid. The amendment blurs that constitutional baseline by allowing future legislation to broaden transaction taxes to any goods and services.

What does “modernize the sales and use tax” really mean?+

In the ballot summary, “modernize” is a friendlier label for expanding the tax base. Voters should read that phrase as shorthand for future legislation that could broaden which transactions are taxed.

Conclusion

This is not a tax cut

At best, this is a constitutional tax-shift framework. It does not automatically eliminate the personal income tax, and it does not itself impose a tax on services. What it does do is rewrite the Constitution so future lawmakers can broaden transaction taxes while relying on revenue-growth promises to eliminate the income tax later.

Even if the plan eventually works as promised, the burden does not disappear — it moves. Missourians who owe little or no personal income tax today could still pay more if lawmakers expand taxes on everyday goods and services. And the talking point that families can simply “control” how much they pay under consumption taxes is not nearly as comforting as it sounds when much of what people buy is necessary, not optional.

The same legislature that has not shown serious spending restraint is asking Missourians to give up constitutional protections and trust them to make the right choices later. The better course is the harder, more honest one: cut spending first, reduce taxes by statute as savings are real, and tell voters the whole truth up front.

Source notes