Which Tax Can You Actually Count?

Rethinking the "transparency" argument for HJR 173.

A quick test for anyone weighing in on Missouri's HJR 173 — the constitutional amendment on the November 2026 ballot.

Prefer to Listen?

Listen to This Article

The full article narrated — about 9 minutes. Includes a quick test you can try as you listen.

Having trouble with the player? Download the MP3 directly.

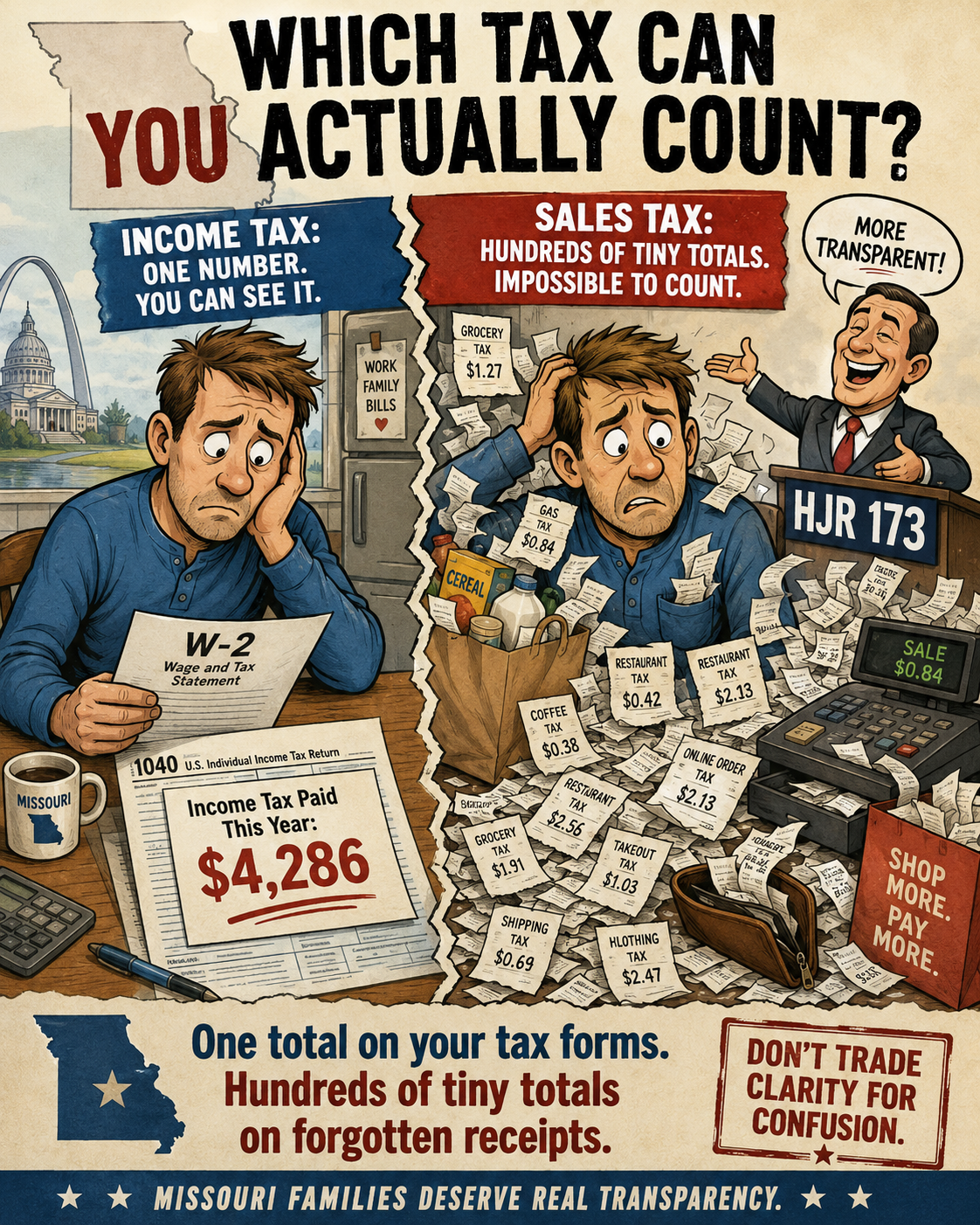

Try This Without Looking

How much did you pay in Missouri state income tax last year? Within $200?

Now: how much did you pay in state and local sales tax last year? Within $200?

Most Missourians can answer the first question. The income tax figure appears in actual dollars on your W-2 every January. It appears again on your 1040 every April. Before that, it shows up on every paystub all year long. By the time the year ends, you've seen the number written down dozens of times. You can quote it within $200 because you've literally read it that many times.

Almost no one can answer the second question. People know the rate is somewhere around 8% combined — about 4.225% state and another 4.22% local on average. But the actual dollar amount? It accumulates across hundreds of grocery runs, gas stops, online orders, restaurant tabs, hardware store purchases, and routine errands. No one adds it up. It never appears as a single number on any document anywhere.

The "Transparency" Argument

Supporters of HJR 173 have made a specific argument for the swap from income tax to expanded sales tax. They call income tax "hidden" — taken out of paychecks before workers see it — and call sales tax "honest" or "transparent" because you can see it at the register.

Sen. Brian Seitz framed it this way in a widely shared post: "The income tax is already in the ham. Dozens of times over. You just can't see it. The consumption tax is honest. The income tax is hidden, and you're paying it whether you know it or not."

Aaron Hedlund, chief economist for domestic policy at the White House Council of Economic Advisors and chief economist at the Show-Me Institute, has made similar arguments. So has Niles Stevens, writing for MO Tax Relief Now: "The income tax is an embedded tax that is still part of what you pay at the register, but it's rolled into the cost."

The framing has surface-level appeal. Sales tax really is visible on your receipt. You see the line that says "tax" and the dollar amount associated with it. That's true.

But it's not how people actually experience the tax over the course of a year.

How People Actually Experience the Two Taxes

Income tax has three documented appearances in every working Missourian's year:

- Every paystub shows the state income tax withholding for that pay period. Most workers see this 26 times a year, or 52 times for weekly pay.

- The W-2 in January shows the total state income tax withheld for the year — a single, prominent dollar figure.

- The 1040 in April shows what was actually owed, what was paid, and the difference (refund or amount due) — also in single, prominent dollar figures.

By the end of any given year, a working Missourian has seen their state income tax expressed as a specific dollar figure dozens of times. That's why most people can answer the first question. The number isn't hidden. It's the most visible single tax figure most Missourians encounter all year.

Sales tax has a different relationship with visibility:

- The receipt at the register shows the tax for that single transaction. A receipt for a $47 grocery run shows the tax — about $4. The receipt usually gets thrown away within 24 hours.

- No annual summary exists. No business sends you a year-end statement of what you paid. The state doesn't issue you a sales tax summary. There is no W-2 equivalent.

- The accumulation is invisible. The $4 from groceries, the $3 from gas, the $1.50 from a coffee, the $12 from a hardware store run — multiplied across hundreds of transactions over twelve months. Almost no one tracks it.

The $4 at any single register feels small. Visible, yes. But the $3,000 to $5,000 a typical Missouri family pays in combined state and local sales tax over a full year — that figure is genuinely invisible. Nobody encounters it as a single number anywhere.

The Inversion

The tax that's "transparent" at the register is the tax that disappears at the annual scale. The tax that's "hidden" in a paycheck is the one people can quantify exactly.

If transparency means knowing what you pay, the income tax is the more transparent tax — by a wide margin.

Why This Matters for HJR 173

HJR 173 is structured as a tax shift. Any new sales tax revenue from base expansion must be offset, in the same legislation, by a substantially-equal income tax reduction. Dollar for dollar. The state ends up collecting roughly the same amount of money. Government doesn't shrink. Its claim on Missourians' resources doesn't shrink. The collection mechanism just changes.

Supporters argue that change is itself a benefit because the new mechanism is more transparent. But the argument runs into the inversion above. Switching from a tax people can see in actual dollars to a tax that vanishes at the annual scale isn't a transparency improvement. It moves Missourians from a tax they can quantify to a tax they can't.

Here's why this matters beyond the surface-level argument. The visibility of a tax shapes how easily citizens can hold legislators accountable for it.

Every spring, Missourians see what they paid in state income tax as a single dollar amount on their 1040. They can compare it to last year. They can decide whether it feels too high. They can call their state representative and complain about a specific number. Campaigns get run on that number. Kitchen-table conversations happen around that number.

Sales tax doesn't generate that kind of accountability moment. People might notice when the rate changes — "I can't believe they raised it" — but they have no equivalent moment of seeing what they paid in total over the year. The $3 here, $7 there, and $12 somewhere else stays invisible at the annual scale. There's no "$4,200 moment" to complain about.

That difference matters politically. A legislator who wants to keep spending faces less constituent pressure on a tax citizens can't easily quantify than on one they see in single-dollar figures every April. The sales tax isn't just less visible to citizens — it's less politically costly for the people deciding how much to take.

If the actual goal of HJR 173 were to make government more accountable to taxpayers, the choice would be to keep the visible tax and reduce the rate through cuts and growth. Trading the visible tax for the invisible one moves accountability in the wrong direction. It makes it easier for government to keep collecting without facing the political friction that comes with citizens knowing exactly what they pay.

HJR 173 isn't transparency reform. It's tax restructuring with a transparency-themed sales pitch.

The Question Underneath

Once the transparency framing falls away, voters are left with the question HJR 173 was always asking: should Missouri restructure how government collects the same amount of money — including expanding sales tax authority to services not currently taxed — or should we reduce what government takes from us in the first place?

Most Missourians want the income tax eliminated. We want that. The disagreement isn't about whether to eliminate the income tax. It's about how — and whether the answer involves giving the legislature new constitutional authority to tax services Missourians use every day.

Cuts-and-growth eliminates the income tax through ordinary legislation, without expanding any sales tax authority, without giving up constitutional protections voters approved, and without trading a tax people can see for a tax they can't.

That's the choice. The transparency argument was the surface. The values question is what's actually on the ballot.

Read More

This is one piece of a larger picture on what HJR 173 actually does. For our full analysis — including the math behind the rate-and-base scenarios, our position on the conservative path forward, and responses to other arguments being made for the amendment — visit our special coverage hub on HJR 173.

The methodology behind our calculations is in our downloadable methodology document — built for voters, journalists, and policymakers who want to verify the work.