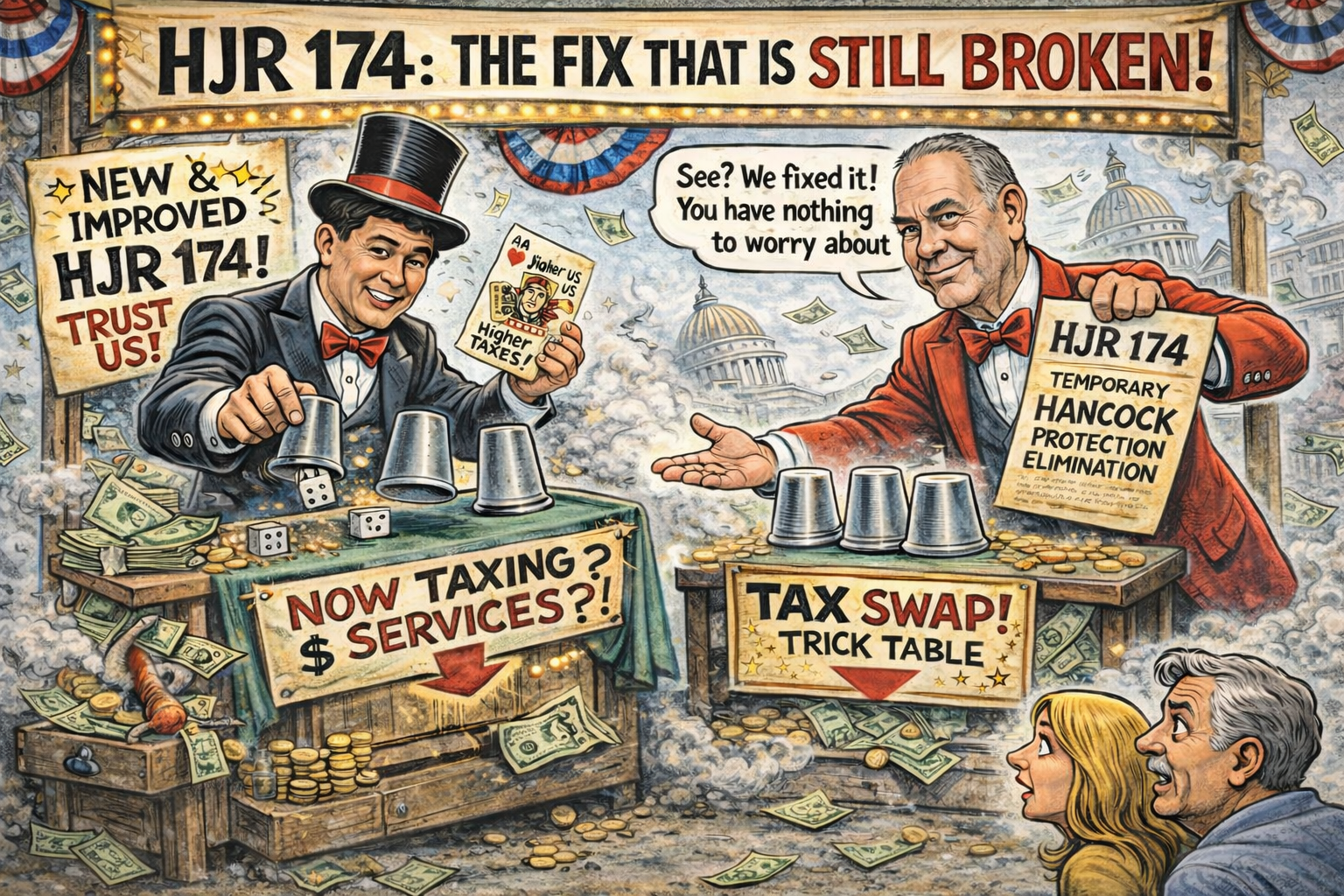

HJR 174: The “Fix” That Still Breaks Hancock

Only a few days after HJR 165 was filed and panned widely, Rep. Jon Patterson filed the “fix” in HJR 174. But it doesn’t fix anything. It still creates a constitutional “tax swap” framework that undermines the Hancock Amendment’s protections and opens the door to taxing everyday services.

Read our full bill analyses

For the provision-by-provision breakdown, see:

Hancock Amendment guide

If “Hancock” feels abstract, we’ve built a citizen-friendly explainer:

Read the Hancock guide act4mo.infoWhat this page does

We translate constitutional language into real-life examples—especially what “taxing services” could mean at the register and on invoices.

We do this in good faith—but the “details” would be written later by legislators.

On this page

What changed from HJR 165

HJR 174 includes drafting cleanups and adds more “structure,” but the underlying mechanism remains the same: weaken Hancock during the swap, eliminate the state individual income tax, and backfill revenue by expanding and increasing sales taxes—potentially onto services.

| Topic | HJR 165 | HJR 174 | Why it matters |

|---|---|---|---|

| Hancock carve-out | Broad carve-outs | Adds a “window” concept (still a carve-out) | A time-limited bypass is still a bypass—especially when it matters most: during implementation. |

| More “moving parts” | Simpler framework | Adds more implementation and administrative mechanisms | More complexity = more discretion, less voter clarity, more opportunities to shift burdens. |

| Local offset language | Less developed | Adds “offset” language to reassure voters | Offsets are not the same as “your family is held harmless.” Some families will pay more. |

What did not change (still the core problem)

- Hancock protections are still being carved up. This is why the “fix” claim is misleading. (If you want a plain explanation of Hancock, see our guide: act4mo.info/guides/hancock-amendment.html.)

- Sales taxes can still be expanded onto services. That is the heart of the “tax swap.”

- Voters are asked to approve a framework first and trust lawmakers later with the details.

- Local earnings taxes remain (and do not disappear even if the state individual income tax is reduced).

New problems in HJR 174

In addition to not fixing the main objections, HJR 174 creates new issues:

- More complexity and more moving parts that are difficult for voters to evaluate.

- Greater uncertainty for small businesses and families because the “how” is deferred to future statutes.

- More opportunities for burden shifting across households based on what they buy (services-heavy households may pay more).

Transparency disclaimer

The examples below are a best-faith attempt to illustrate potential impacts if Missouri expands sales tax to services. We cannot know today exactly which services future legislators will tax (or exempt), what rate structure they will choose, or how local jurisdictions will respond. That uncertainty is a core concern: the constitution would be amended first, while the real “what gets taxed” decisions come later.

What this could mean for citizens: interactive examples

Most Missourians don’t read bill text. They read receipts and invoices. The tool below helps people see: (1) what they might save if the Missouri individual income tax goes to $0, and (2) what they might pay if services become taxable at their local combined rate.

Before you use the calculator, scan the list of services below. The point is simple: if lawmakers start applying sales tax to services, it wouldn’t just affect “optional” spending — it could hit routine parts of family life like child care, auto repairs, home maintenance, and personal care.

Those added taxes can quietly eat away at any savings from eliminating the Missouri individual income tax over the course of a year. And if you have one or two major service expenses (a transmission, a new roof, HVAC replacement, major plumbing), the added tax on that single bill can wipe out a large chunk of your annual income-tax savings all at once.

Services You Might Not Expect to Be Taxed

If lawmakers expand sales tax to “services,” it could reach far beyond retail purchases. These are examples Missourians often don’t think about—until the bill shows up.

Family & Kids

- Child care / daycare / after-school care

- Tutoring, test prep, music lessons

- Summer camps and youth programs

- Sports training / dance classes

Home & Housing

- HVAC, plumbing, electrician service calls

- Appliance repair and handyman work

- Pest control and termite treatments

- Landscaping, tree trimming, lawn care

- Moving services and junk removal

Auto & Transportation

- Auto repair labor (diagnostics, transmission, brakes)

- Towing and roadside services

- Car wash / detailing

- Delivery/ride-share service fees

Personal Care

- Haircuts, salon services, nails

- Massage therapy and spa services

- Gym memberships and personal training

- In-home care services (elder care)

Professional Services

- Tax preparation / CPA services

- Legal services (wills, contracts, closings)

- Bookkeeping and payroll services

- Financial advising fees

Digital Life

- Software subscriptions (accounting, design, CRM)

- Web hosting, website maintenance

- IT support and cybersecurity services

- Phone/computer repair services

Why we’re showing this list

The point is not to claim every item will be taxed. The point is that once the constitution is amended, the Legislature can define “taxable services” later—often in ways citizens won’t see coming until it hits their household bills.

Now use the estimator to see the trade-off in a way that feels real: (1) it estimates what you pay in Missouri state individual income tax today, and (2) it estimates what you might pay in added tax if a sales tax were applied to the kinds of services listed above (at a combined rate similar to your local sales tax rate).

The break-even number is the most important concept to understand. It shows how much you could spend in a year on newly-taxed services before the added sales tax equals your income-tax savings. Once your annual service spending reaches that break-even amount, you are no longer coming out ahead — any additional taxable services above that level mean you would pay more overall than you saved from eliminating state income tax.

Tip: If you’re unsure what to enter, start with the “Preset” buttons. They are not predictions — they are examples designed to illustrate how quickly service taxes can add up in the real world.

Important clarification

These estimates relate to Missouri state taxes only. Eliminating Missouri’s individual income tax would have no impact on what you pay in federal income tax to Uncle Sam.

Your federal withholding and federal tax bill would still apply.

Step 1 — Income tax estimate (today)

Enter your Missouri taxable income. If married filing combined, Missouri calculates tax for each spouse separately and adds them.

Show the Missouri income-tax bracket table used in this estimator

This uses the Missouri individual rate chart with a top rate of 4.7%. The exact thresholds can change over time; adjust as needed if DOR updates the chart.

| MO taxable income | Tax |

|---|---|

| $0 – $1,348 | $0 |

| $1,348 – $2,696 | 2.0% of excess over $1,348 |

| $2,696 – $4,044 | $27 + 2.5% of excess over $2,696 |

| $4,044 – $5,392 | $61 + 3.0% of excess over $4,044 |

| $5,392 – $6,740 | $101 + 3.5% of excess over $5,392 |

| $6,740 – $8,088 | $148 + 4.0% of excess over $6,740 |

| $8,088 – $9,436 | $202 + 4.5% of excess over $8,088 |

| Over $9,436 | $263 + 4.7% of excess over $9,436 |

Step 2 — “If services were taxed” estimate

Pick a combined sales tax rate to illustrate what your receipts could look like if services are taxed. (Missouri rates vary by location; use a realistic value for your area.)

Choose example services (editable)

Results

Break-even spending

You “break even” when newly-taxed service spending reaches:

$0

If you spend more than this on newly-taxed services in a year, the added sales tax will exceed what you save from eliminating the Missouri individual income tax.

Why this matters

Even if your income tax drops, a broad services tax can show up exactly when families can least afford it: child care, repairs, and essential services.

Quick “receipt math” tool

Want a fast way to show people what a services tax could look like? Put in an invoice amount and a combined rate. This produces the extra tax and the new total.

Try: 35 haircut, 250 plumber, 1500 water heater, 6000 transmission

Use your local combined rate

Added tax

$21.25

Total bill with tax: $271.25

Why we’re calling this a “fix” that isn’t a fix

If you support tax cuts, you should insist on reforms that are transparent, written as a single subject, and that do not weaken Hancock protections.

- The Hancock Amendment exists to restrain government revenue growth. If lawmakers can step around Hancock during a “tax swap,” that’s when the guardrail is needed most. (See our guide: Hancock Amendment explainer.)

- Taxing services shifts the burden toward consumption and everyday family life.

- Constitution first, details later is backwards — voters deserve to know what gets taxed before voting.

Want the full provision-by-provision breakdown?

Use our official analyses here: