Following the Ham: What "The Income Tax Is Already in the Price" Leaves Out

A response to a popular HJR 173 argument now circulating among Missouri legislators and supporters of the amendment.

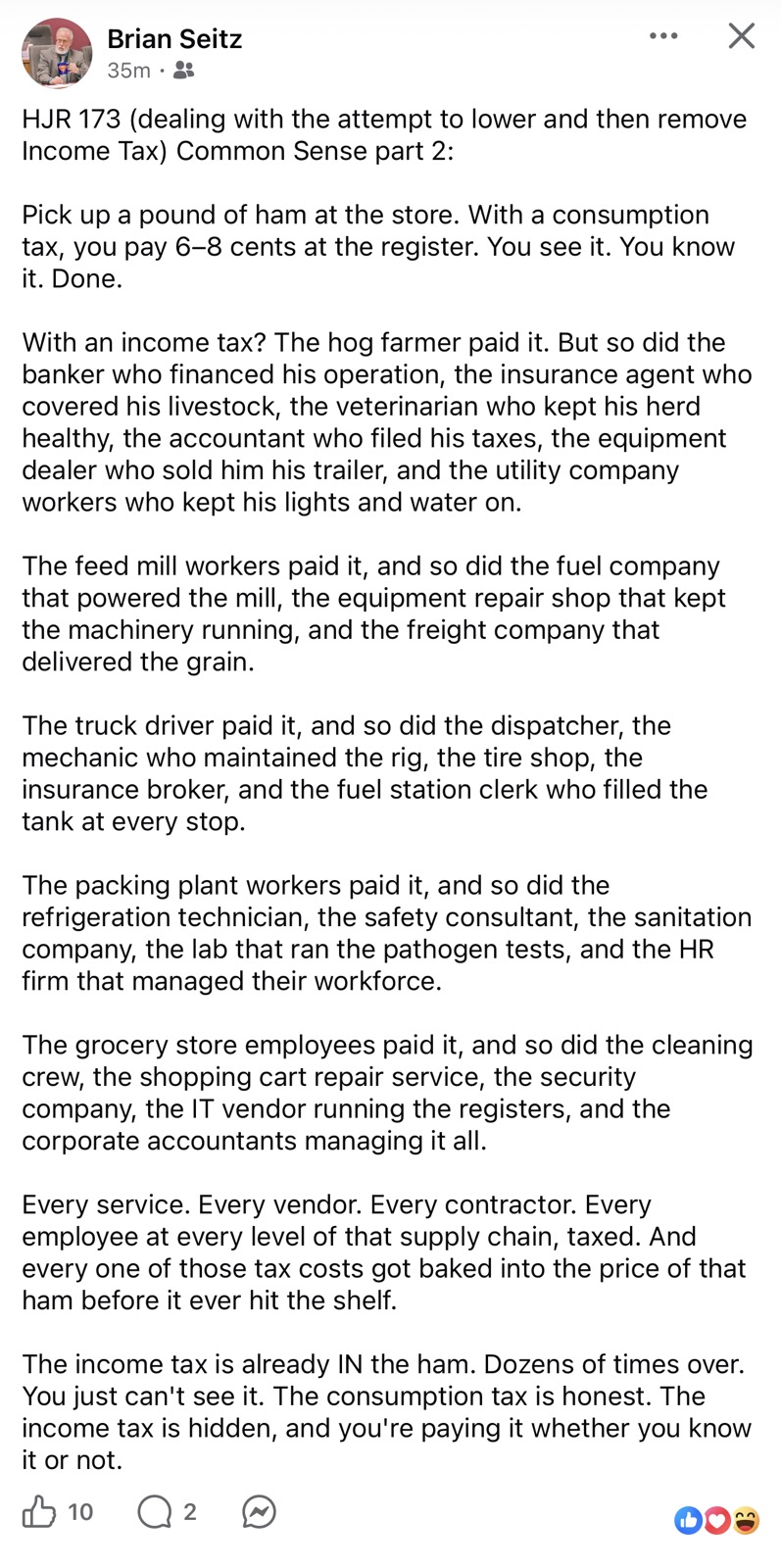

A vivid argument for HJR 173 has been making the rounds on social media and in conversations with constituents. It goes like this: when you buy a pound of ham, the income tax is already baked into the price — paid by the farmer, the banker, the veterinarian, the truck driver, and everyone else in the supply chain. So switching to a consumption tax just makes a hidden tax visible. The income tax, the argument concludes, is already in the ham.

The economics behind this argument has a kernel of truth, and it's worth taking seriously rather than dismissing. But the argument leaves out four things that change the conclusion significantly. Once you put those things back in, the same pound of ham tells a very different story.

Prefer to Listen?

Listen to This Article

The full article narrated — about 20 minutes. Great for commutes or anytime you'd rather hear it than read it.

Having trouble with the player? Download the MP3 directly.

The Argument Being Made

Here's the post that's been widely shared, from State Senator Brian Seitz, as a representative example of how the argument is being framed:

The argument is rhetorically powerful, and the underlying economics is real. Public finance has documented for decades that taxes paid throughout supply chains do get factored into business costs, which feed into prices. Economists call this tax incidence — the difference between who legally pays a tax and who actually bears its economic cost. Some portion of business and individual income taxes does flow through to consumer prices. We're not disputing that.

But the leap from "some income tax is embedded in prices" to "switching to a consumption tax is just making a hidden tax visible" requires several things to be true that aren't. Let's walk through what the argument leaves out.

HJR 173 Only Eliminates a Small Slice of the Tax in the Ham

The argument lists everyone in the supply chain — the farmer, the banker, the veterinarian, the accountant, the truck driver, the packing plant workers, the grocery store employees — and says they all paid income tax that's now in the price of ham. That's true.

But every one of those people is paying multiple taxes, and HJR 173 only eliminates one of them: Missouri's state personal income tax. Everyone in that supply chain still pays:

- Federal income tax (10% to 37% marginal, often a larger share of their tax burden than state income tax)

- Federal payroll taxes (15.3% combined Social Security and Medicare, with half visible on the paycheck and half hidden in the employer's labor cost)

- Federal corporate income tax on the businesses that employ them (21% on C-corporations)

- Property taxes on every business facility in the chain — the farm, the feed mill, the trucking depot, the packing plant, the grocery store

- Federal excise taxes on the fuel that powers the trucks and the equipment

- Various business license fees and regulatory taxes

Missouri's top state income tax rate is 4.7%, and it kicks in only on income above $9,191. For most workers in the supply chain, the effective state income tax rate on the marginal dollar is somewhere between 3% and 4%. Compared to the other taxes flowing through that supply chain, state personal income tax is a small slice of the embedded burden, not the whole thing.

What this means for the ham

Eliminating state personal income tax doesn't unwind all the hidden tax in the price. It removes a sliver. The federal taxes, payroll taxes, business taxes, and property taxes that make up the larger portion of the embedded tax burden continue exactly as before. The ham still has most of those taxes baked into it.

The Sales Tax Doesn't Replace the Income Tax — It Gets Added On Top

The original argument treats the swap as conserved: hidden income tax in the ham gets replaced by visible consumption tax at the register. Same money, different mechanism.

That isn't what HJR 173 actually does. The amendment doesn't remove the existing sales tax. It keeps the current 4.225% state rate plus the average 4.22% local rate, and gives the legislature the constitutional authority to add new sales tax revenue on top of the existing structure. The math we worked out in our main HJR 173 analysis shows that even in the most optimistic scenario for proponents, the combined state-and-local sales tax rate ends up higher than today, not the same.

So what actually happens to the price of that pound of ham?

| Tax Component | Current Law | Under HJR 173 |

|---|---|---|

| Federal income tax in the supply chain | Embedded in price | Still embedded — unchanged |

| Federal payroll taxes in the supply chain | Embedded in price | Still embedded — unchanged |

| Federal corporate income tax | Embedded in price | Still embedded — unchanged |

| Property taxes on businesses in chain | Embedded in price | Still embedded — unchanged |

| Missouri state personal income tax in chain | Embedded in price (small portion) | Gone — eventually |

| Sales tax at the register | ~8.4% combined (reduced rate on groceries) | Higher rate, possibly higher base |

| New sales tax on services in supply chain | None on most B2B services | Possible — embedded in price |

The honest accounting

HJR 173 doesn't replace hidden tax with visible tax on a one-for-one basis. It removes a small slice of the hidden tax (state personal income tax), leaves the larger hidden taxes alone (federal income tax, payroll taxes, corporate taxes, property taxes), and adds a new visible tax on top — at potentially higher combined rates than today.

Businesses Don't Pass Tax Savings Through Dollar-for-Dollar

The argument implies that if state income tax is eliminated, the price of the ham will drop by the embedded amount — that consumers will see in lower prices what's no longer being paid in income tax. But that's not how pricing actually works.

When business costs decrease — whether through tax cuts, lower input costs, or efficiency gains — empirical research shows the savings get distributed across multiple destinations. Businesses can use them for higher profits, higher wages, capital investment, debt reduction, or lower prices. Lower prices is typically the smallest share of where cost savings go, and it usually takes time to materialize even when it does happen.

Pricing is set by what the market will bear, not by a precise accounting of input costs. If the price of ham is currently set at what consumers will pay, removing a small portion of input cost doesn't automatically reduce that price. Businesses pocket some, share some with workers, invest some — and may pass a small portion through to consumers, eventually.

Meanwhile, the new sales tax at the register is immediate, transparent, and one-to-one. The 6 to 8 cents — or considerably more, depending on which scenario plays out — gets added to your purchase the day the law takes effect.

What this means for the ham

The hidden tax savings, if they materialize for consumers at all, arrive slowly and partially. The new visible tax arrives immediately and fully. The trade is not symmetric.

Tax Cascading Adds More Hidden Tax — Not Less

Here's where the argument's own logic turns against it. When you tax services that businesses buy from each other, the tax gets embedded in those services, which gets embedded in the next product, which gets taxed again at the register. Economists call this tax pyramiding or cascading. It's the reason most public finance literature recommends exempting business-to-business services from consumption tax bases.

Walk through the original argument's supply chain again, but this time apply HJR 173's expanded sales tax to the services those businesses buy:

- The hog farmer hires a veterinarian. Under expansion, the vet's services are taxed. That tax goes into the cost of producing the hogs.

- The hog farmer hires an accountant. Under expansion, that's taxed too. Adds to the cost.

- The trucking company pays for equipment repair. Taxed. Cost goes up.

- The packing plant uses HR services, lab testing, refrigeration maintenance. All potentially taxed. All costs up.

- The grocery store pays for IT services, security, cleaning, accountants. Taxed. Adds to overhead.

Every one of those new taxes gets embedded in the price of the ham. By the time the ham reaches your shelf, it has accumulated tax not just at every income-earning step (which still happens) but also at every service-purchasing step. And then it gets taxed again at the register.

The amendment doesn't prohibit taxing business-to-business services. In fact, the broad base expansion that supporters acknowledge is needed to keep the rate near 6% almost certainly requires reaching into B2B services to make the math work.

What this means for the ham

The original argument says income tax in the supply chain is "in the ham." Under HJR 173, that doesn't go away — and a new layer of embedded tax gets added to it through cascading. The ham ends up with more hidden tax in its price than it has today, plus a higher visible tax at the register.

The Ham Example Picks the Best Case for the Argument

There's one more thing worth noticing about the framing. The argument uses ham — food — as the example. That's a sympathetic choice for the argument, because Missouri currently taxes groceries at a reduced rate (1.225% state instead of 4.225%, with local taxes still applying on top). So the visible sales tax on a pound of ham at the register today is genuinely small. Adding a few more cents looks modest by comparison.

But what about the things HJR 173 would actually have to start taxing to make the math work? The amendment authorizes the legislature to expand the sales tax base to services not currently taxed. Run through the same exercise with examples that aren't taxed today at all:

- Your monthly rent. Currently no sales tax. Under broad expansion, taxed at potentially 9% combined or more. On a $1,200 rent payment, that's $108 per month, $1,296 per year.

- A doctor's visit. Currently no sales tax. Under broad expansion, taxed. On a $200 office visit, that's $18 added.

- Your child's daycare. Currently no sales tax. Under broad expansion, potentially taxed. On $1,000 monthly daycare, that's $90 per month, $1,080 per year.

- Hiring a real estate agent or closing on a house. Currently no sales tax on the services. Under broad expansion, taxed.

- Legal services, accounting services, professional services. Currently mostly untaxed. Under broad expansion, taxed.

For these categories, the original argument's logic falls apart entirely. There's no embedded "hidden income tax" being made visible — these services were never subject to a state-level transaction tax in the first place. HJR 173 isn't unveiling a hidden tax on rent, healthcare, or daycare. It's creating a brand-new tax on them.

What this means for Missourians

The "ham" framing works as rhetoric because food has a small visible tax to begin with, and a relatively transparent supply chain. But Missourians don't only buy ham. They pay rent, see doctors, send kids to daycare, hire professionals, and use services every day that have no current sales tax. Under HJR 173, those bills would carry a new tax that didn't exist before — with no offsetting "hidden" tax being unveiled.

The Honest Accounting: What Actually Happens to the Ham

Pull all five points together and walk through the same pound of ham one more time, this time honestly.

Under current law, the ham carries embedded federal income tax, federal payroll taxes, federal corporate tax, property taxes, and a small slice of state personal income tax from the supply chain. At the register, you pay a reduced sales tax on groceries — currently around 5.45% combined.

Under HJR 173, the ham carries the same embedded federal income tax, the same federal payroll taxes, the same federal corporate tax, the same property taxes, plus possibly new embedded sales taxes from services purchased throughout the supply chain. At the register, you pay a sales tax that may be higher than today depending on the rate-and-base scenario, possibly without the reduced rate for groceries that exists today.

The state personal income tax sliver is gone. Everything else continues, plus new things get added.

That isn't the simpler tax structure the argument promises. It's the same hidden tax burden minus a small slice, plus a higher visible tax, plus potentially new hidden taxes from cascading. The pound of ham doesn't get cheaper. The tax structure doesn't get more honest. It gets more expensive and more complicated, while a small piece of state-level income tax goes away.

"The Consumption Tax Is Honest" — A Closer Look

The original argument lands its conclusion on a memorable line: "The consumption tax is honest. The income tax is hidden, and you're paying it whether you know it or not."

Visibility of taxation is a legitimate value. Voters arguably should be able to see what they're paying. But that argument doesn't actually favor consumption taxes over income taxes — it favors all taxes being visible.

And there's a more direct point worth making: a paystub shows state income tax withholding clearly. It's right there on the line item. Every Missourian who has ever filed a W-4 has seen the state income tax line. The "hidden" framing applies to corporate income taxes embedded in business prices through the supply chain — but most of that is federal corporate income tax, not state. HJR 173 doesn't touch the federal taxes that make up the bulk of the embedded burden.

If hidden taxation is genuinely the problem, the conservative answer is to make all taxes visible. Tennessee, for example, requires line-item disclosure of sales taxes on receipts above a certain amount. That's a real transparency reform. Adding a new visible tax while leaving the larger hidden ones in place isn't transparency reform — it's tax restructuring with a transparency-themed sales pitch.

The Bottom Line on the Ham

The "income tax is already in the ham" argument has a kernel of economic truth, but it's wrapped around a misleading conclusion. Under HJR 173:

- The hidden income taxes don't go away. Only a small slice (state personal income tax) does.

- Federal income taxes, payroll taxes, corporate taxes, and property taxes continue to flow through into prices exactly as they do today.

- A new, higher visible sales tax gets added on top — potentially with new embedded taxes from cascading through B2B services.

- Items that aren't taxed today — rent, healthcare, daycare, professional services — could face a new tax that didn't exist before.

The honest description isn't "consumption tax replaces hidden income tax." It's "a new visible tax gets added on top of an existing tax burden that mostly stays in place, while a small portion of state-level income tax goes away over time." Voters deserve to evaluate HJR 173 on those actual terms, not on a rhetorical frame that obscures what the amendment actually does.

Want to verify the math?

Download Our Methodology Document

A two-page PDF showing exactly how we calculated every figure in our HJR 173 analysis — with sources, assumptions, and step-by-step arithmetic. Free to share, print, and republish.

Where Act for Missouri Stands

Act for Missouri supports eliminating Missouri's individual income tax. We've been clear about this in our broader work, and we believe many Missourians across the political spectrum could agree on that goal. The disagreement isn't about whether to eliminate the income tax — it's about how.

HJR 173 eliminates the income tax through tax shifting, not actual tax reduction. A better path is available: the Senate's claimed $4.11 billion in budget cuts, combined with reasonable economic growth, covers most of the $8.51 billion in income tax revenue that needs replacement. With Republican supermajorities in both chambers and a Republican Governor, this is the rare moment when elimination through spending discipline is actually achievable. That path doesn't require asking voters to authorize a constitutional framework whose specifics arrive later. It doesn't create new taxes on rent, healthcare, childcare, and services Missourians use every day. And it preserves something Missouri has that the other no-income-tax states don't: a genuinely low cost of living.

For a deeper look at the math behind these claims, see our methodology document. For the full analysis of HJR 173, see our main article.

What You Can Do

If you've seen the "income tax is already in the ham" argument shared by a friend, family member, or legislator, share this article in response. The economics deserves engagement on its own terms — not dismissal — and Missourians deserve to evaluate HJR 173 on what it actually does, not on a frame that obscures the trade-off.

Use the legislator lookup tool at the top of this page to find your state senator and representative. Tell them what you think about HJR 173, the rate math, and the path to income tax elimination Missouri is uniquely positioned to take. Ask them where they stand on the cuts-and-growth alternative.

The November 2026 vote is approaching. The conversation between now and then will shape how Missourians understand the most consequential tax restructuring in state history. Your voice in that conversation matters.